In the realm of finance, there’s a concept as fundamental as gravity is to physics – interest. It permeates every financial transaction, from the everyday act of swiping your credit card to the complex world of stock market investments. But what exactly is interest, and how does it influence our financial decisions? Buckle up, because we’re about to delve into the fascinating dance of interest in borrowing, lending, and investing.

Demystifying Interest: The Cost of Borrowing and the Reward of Lending

Interest, the fundamental concept that fuels borrowing, lending, and investing, goes beyond a simple price tag. It’s a dynamic force that influences financial decisions across the spectrum, from everyday transactions to complex investment strategies. Let’s delve deeper into the intricacies of interest and its role in various financial scenarios.

Understanding the “Why” Behind Interest Rates:

The concept of interest boils down to the time value of money. Money today is worth more than the same amount of money in the future, due to the potential for it to grow through investment or inflation. Imagine you lend a friend $100 today. A year later, they could potentially use that money to earn a return, say through interest on a savings account. So, it’s fair to expect some compensation for giving them access to your money for that period. This compensation, expressed as a percentage (interest rate), reflects the time value of money and the risk associated with the loan.

The Symphony of Factors Affecting Interest Rates:

Several key players influence the interest rate you pay or receive:

- Risk: Lenders naturally charge higher interest rates to borrowers perceived as riskier. This risk assessment considers factors like credit score, income stability, and the purpose of the loan. A borrower with a poor credit history might be seen as more likely to default, leading to a higher interest rate to compensate for the increased risk.

- Inflation: Interest rates need to account for inflation, the gradual increase in prices over time. If you lend someone money at a 3% interest rate, but inflation is 4%, you’re actually losing purchasing power because the money you get back will buy less than it did when you loaned it. To compensate for inflation, lenders typically set interest rates higher than the prevailing inflation rate.

- Supply and Demand: Just like any good or service, interest rates are influenced by the supply and demand for loanable funds. Think of banks acting as intermediaries. When there’s a surplus of money available for loans (high supply), interest rates tend to be lower as banks compete for borrowers. Conversely, when there’s a high demand for loans and a limited supply of funds, interest rates rise as banks can charge borrowers more.

- Government Policy: Central banks, like the Federal Reserve in the US, play a crucial role in influencing interest rates. By raising or lowering interest rates, they can stimulate economic activity or control inflation. For example, if the economy is sluggish, the central bank might lower interest rates to encourage borrowing and spending, which can boost economic growth.

Beyond the Basics: Different Types of Interest:

The world of interest goes beyond a single rate. Understanding these variations is crucial for making informed financial decisions:

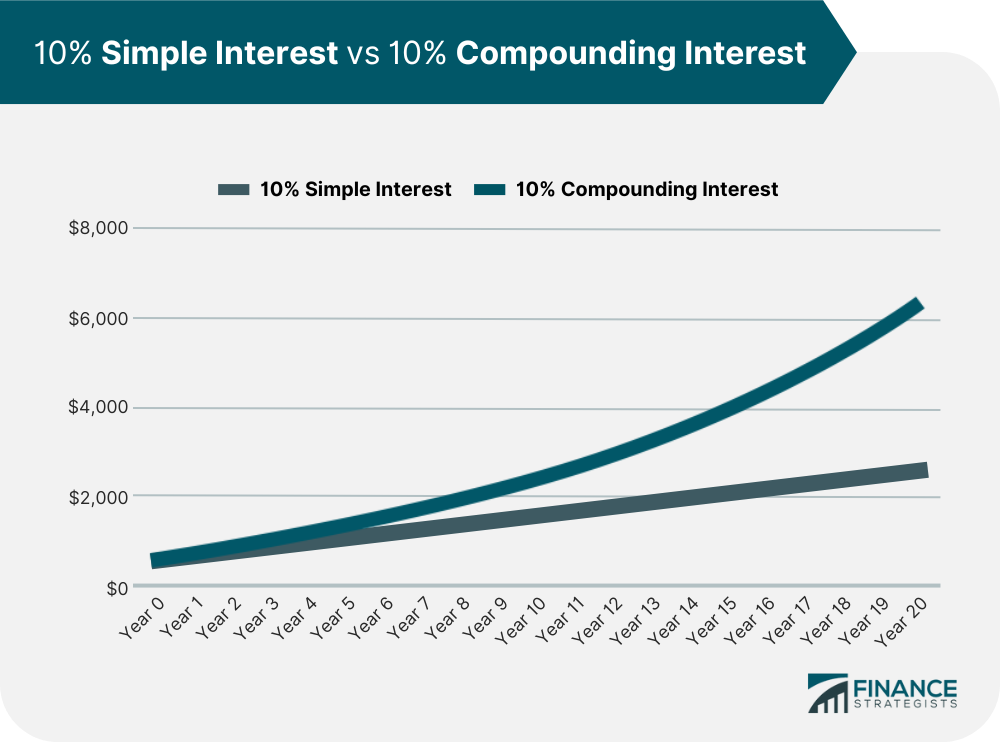

- Simple vs. Compound Interest: Interest, the cornerstone of finance, comes in two flavors: simple and compound. While both represent the cost of borrowing or the reward of lending, their calculations lead to vastly different outcomes. Let’s delve into the world of simple and compound interest to understand their key differences and their impact on your financial decisions.

- Simple Interest: A Straightforward Calculation

Imagine borrowing $1,000 from a friend at a 5% annual interest rate. Simple interest is calculated by multiplying the principal amount (the initial $1,000) by the interest rate (5%) and the time period (number of years). In this case, after one year, the interest owed would be:

Interest = Principal x Interest Rate x Time

Interest = $1,000 x 5% x 1 year = $50

Therefore, you’d repay your friend the original $1,000 borrowed, plus the $50 in interest, for a total of $1,050.

- Compound Interest: The Power of Growth on Growth

Now, let’s explore the magic of compound interest. Here, interest is calculated not just on the original principal amount, but also on any accumulated interest. Imagine the same scenario as before, but with compound interest. After one year, you’d still owe $50 in interest. However, in the second year, the interest would be calculated on the total amount owed, which is $1,050.

Year 2 Interest = ($1,000 + $50) x 5% = $52.50

This snowball effect, where interest earns interest, can lead to significant growth over time. While the difference might seem small in the beginning, the power of compounding becomes evident in the long run.

- Fixed vs. Variable Interest Rates: Fixed interest rates remain constant throughout the loan term, offering predictability for borrowers. Variable interest rates fluctuate based on a benchmark rate, such as the prime rate. This can be beneficial if the rate goes down, but also carries the risk of higher payments if the rate increases.

Interest in Action: Practical Examples:

Let’s see how interest plays out in real-life scenarios:

- Borrowing a Car: When you take out a car loan, you’re essentially borrowing money from a bank to purchase a car. The interest rate you pay will depend on factors like your creditworthiness, the loan term, and the prevailing market interest rates.

- Investing in a Savings Account: When you deposit money in a savings account, you’re essentially lending your money to the bank. In return, the bank pays you an interest rate on your deposit. While the interest rate on savings accounts is typically low, it offers some return on your money and keeps it readily accessible.

- Buying a Bond: Bonds are essentially loans you make to a government or corporation. They pay a fixed interest rate (coupon) at regular intervals and return the principal amount at maturity. The interest rate on a bond is influenced by factors like the creditworthiness of the issuer and the prevailing market interest rates.

The Investor’s Game: Interest Rates and Investment Decisions

When interest rates are low, the potential for higher returns from stocks can be more attractive, potentially leading to increased investment in the stock market. This is because the returns offered by traditional interest-bearing accounts like savings accounts and CDs become less competitive. Investors seeking higher returns might be willing to accept the inherently higher risk associated with stocks in pursuit of greater potential gains.

However, rising interest rates can create a different dynamic in the investor’s game. As interest rates climb, the allure of bonds increases. Bonds typically offer fixed interest payments, and when prevailing interest rates rise, the value of existing bonds with lower interest rates can actually decrease. However, newly issued bonds will offer the more attractive, higher interest rates, making them more appealing to investors. This can lead to a shift in investment strategies, with some investors moving funds out of the stock market and into bonds to secure higher and more predictable returns.

Here’s how understanding the relationship between interest rates and investments can empower you as an investor:

- Asset Allocation: Interest rates are a key factor when determining your asset allocation, which is the strategy of dividing your investment portfolio among different asset classes like stocks, bonds, and cash equivalents. When interest rates are low, a higher allocation to stocks might be appropriate, while a rising interest rate environment might suggest increasing your bond allocation to balance your risk profile.

- Market Volatility: Interest rate changes can also impact market volatility. When interest rates are low, the stock market can become more volatile as investors chase returns. Rising interest rates, on the other hand, can sometimes lead to increased market volatility as investors adjust their portfolios and react to the changing economic landscape.

- Understanding Bond Duration: When interest rates rise, bonds with longer maturities (the time until the bond matures and the principal is returned) are typically impacted more significantly than short-term bonds. This is because longer-term bonds lock you into a lower interest rate for a longer period. Understanding bond duration and the potential impact of interest rate changes can help you make informed investment decisions within the fixed-income portion of your portfolio.

The Bottom Line:

Interest rates are a powerful force shaping the investment landscape. Understanding how they influence different asset classes and investor behaviour can equip you to make informed decisions and navigate the ever-evolving world of finance. Remember, there’s no single “right” investment strategy. By considering your risk tolerance, financial goals, and the current interest rate environment, you can tailor an investment approach that maximises your long-term returns while managing your risk exposure effectively.